The tech sector usually hogs the AI spotlight. However, there’s another overlooked sector that has been heavily relying on artificial intelligence for cost savings, increased productivity, and error reduction: financial firms.

Banks, insurers, and investment firms are sitting on mountains of data, operate in high-volume environments, and face constant pressure to cut costs while improving customer experience. That's basically AI’s sweet spot.

But the real question isn’t whether financial firms are using AI (because, of course, they are!); it’s where they’re deploying it, what results they’re actually seeing, and where the money is being wasted.

I analyzed earnings reports, press releases, investor day presentations, and industry surveys across banking, insurance, investment management, and payments to see how financial firms are using AI. Here's what I found.

{toc}

TL;DR: A summary of how the top financial firms are using AI

Here’s a quick table summarizing how the big financial firms are using AI:

Firm

Biggest AI win

Workforce impact

ROI

JP Morgan

Cost-neutral on AI spend—saves $2B/year from fraud detection, coding efficiency, and operations automation. 250K employees use LLM Suite weekly

Plans 10% operations reduction over 5 years even as volumes grow 25%. Added 2,000 employees overall in 2025

Breaking even

Bank of America

Erica for Employees used by 90%+ staff, cut IT calls by 50%

Hired just 2,000 from 200K recent grad applicants (1% acceptance)

Not publicly shared, but productivity gains are significant

DBS Bank

370 AI use cases across 1,500+ models

No mass cuts

$1 billion in value from AI initiatives

Lloyd Banking Group

Athena (internal AI) serves 20K employees, cutting search times 66%

No headline layoff numbers tied to AI specifically

£50 million ($68.7 million) of value in 2025 from AI

Citigroup

AI automates code reviews, freeing up 100,000 developer hours a week

Cutting 20K jobs by end of 2026 (~8% of workforce)

No specific dollar ROI disclosed

The biggest benefit of all: AI in fraud detection

By far the biggest boon for humanity is the ability to detect and spot fraud early, thanks to AI. But fraud detection isn’t just good for us; it’s also a revenue protector for financial firms.

The U.S. Department of the Treasury announced that it recovered $4 billion in fraudulent and improper payments in fiscal year 2024—a six-fold increase from $652.7 million in 2023.

“We’ve made significant progress during the past year in preventing over $4 billion in fraudulent and improper payments. We will continue to partner with others in the federal government to equip them with the necessary tools, data, and expertise they need to stop improper payments and fraud,” said Deputy Secretary of the Treasury Wally Adeyemo.

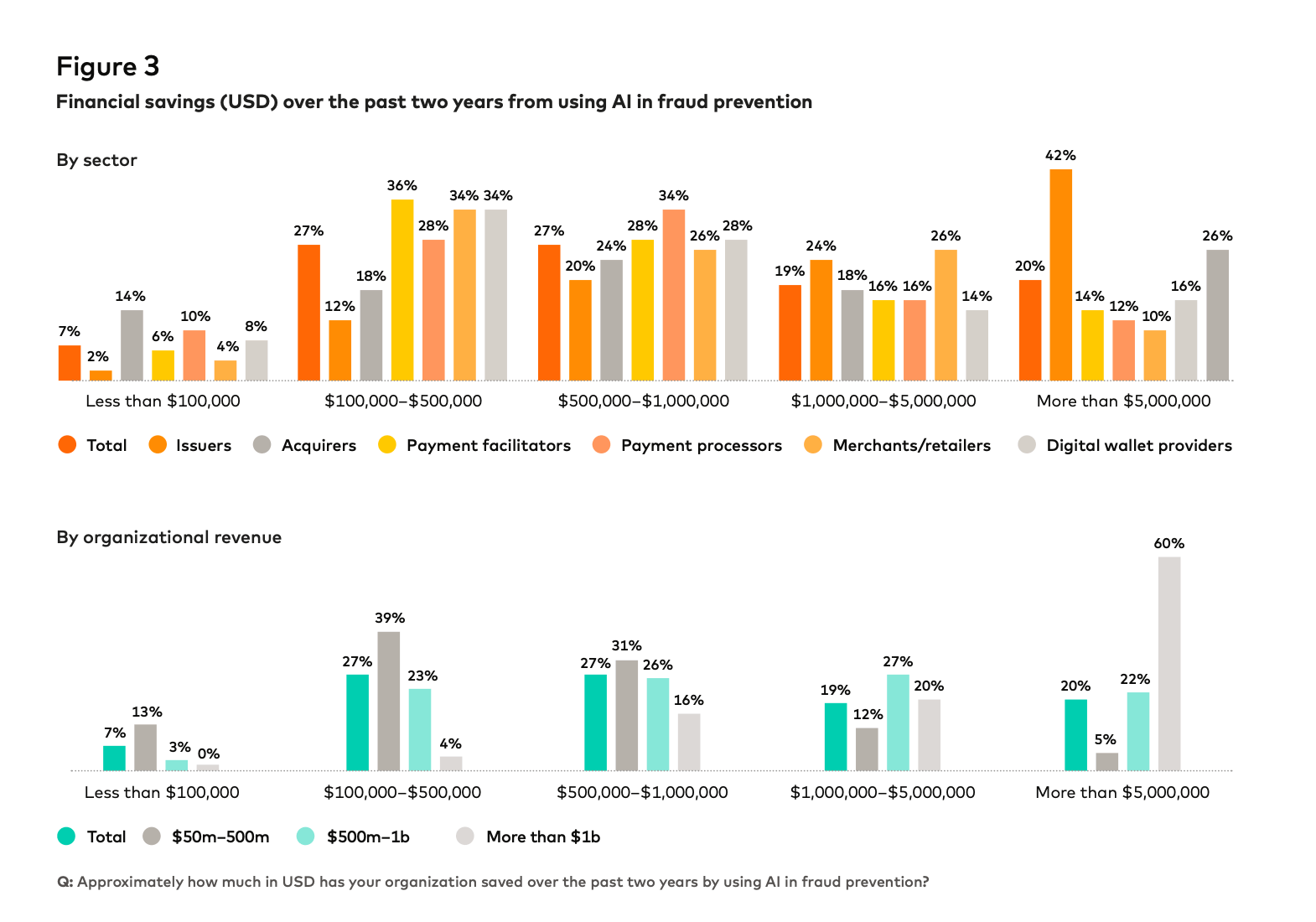

While the Treasury's approach here is mostly traditional machine learning (anomaly detection, risk scoring, cross-referencing databases, etc.), according to Feedzai's 2025 report, 90% of financial institutions now use genAI for fraud detection, with two-thirds adopting these tools within just the past two years.

And the results are promising already:

- Visa saved nearly $40 billion in fraudulent transactions globally in 2023 with its AI systems, trained on 15 billion VisaNet transactions. The company also launched a generative AI-powered VAAI Score to identify enumeration attacks—a type of card testing fraud causing $1.1 billion in annual losses.

- Mastercard doubled its fraud detection rate for fraudulent cards using generative AI and graph technology. Its 2025 survey shows 42% of issuers saved over $5M in fraud losses over two years thanks to AI.

- HSBC, working with Google Cloud, uses AI to monitor 900 million transactions monthly across 40 million accounts. The system reduced false positives by 60% and detected two to four times more financial crimes (with greater accuracy).

- Insurance firms are seeing results, too. AXA Switzerland stopped over €12M in fraudulent payouts, and Zurich Insurance claims to save £260,000 in false claims every day.

Takeaway: Fraud detection in financial firms is the one area where AI has an unambiguous, proven ROI. Traditional ML still does the heavy lifting for transaction monitoring, but generative AI is increasingly layered on top for things—like explaining risk scores to analysts, detecting deepfakes, and synthesizing fraud case profiles faster.

AI agents (and chatbots) are helping financial firms save millions (in time and money)

“AI agents” has become a catch-all term in finance, but not everything labeled an “agent” is actually one. A chatbot that answers HR questions from a database is useful, but it's not an agent. An agent acts autonomously—it executes multi-step workflows, makes decisions within guardrails, and takes action without being prompted at every step.

That distinction matters because the ROI story is very different. Chatbots save time on repetitive queries. Agents transform how work gets done.

JP Morgan was one of the first firms to share its now cost-neutral in its AI investment—investing $2 billion and getting the same in return. How does that $2 billion in savings break down? JPMorgan hasn't released a full accounting, but here's what we know from public statements:

- Fraud detection: The company has reduced its losses by identifying fraud and detecting suspicious activity early. Their Project AIKYA exclusively focuses on spotting anomalies in transactions using AI. According to TigerGraph, JP Morgan also used their graph technology to save $50M a year in operational savings and detect frauds more accurately.

- Software development: Engineering teams using JP Morgan’s internal coding assistants see 10-20% efficiency gains.

- Operations: In the 2025 Investor Day transcript, JP Morgan told investors that operations and support staff would fall by at least 10% over five years—even as business volumes grow by over 25 percent—thanks to AI.

- Client service and research: About 250,000 employees use the LLM Suite weekly for research, report summarization, and contract analysis. The suite generates investment banking presentations in ~30 seconds—work that used to take hours.

“Every employee will have their own personalized AI assistant; every process is powered by AI agents, and every client experience has an AI concierge,” says the Chief Analytics Officer, Derek Waldron.

Beyond JPMorgan, most large banks have deployed AI tools for employees, but they fall on a spectrum from simple chatbots to genuine agentic systems.

Closer to chatbots (useful, but not agents):

- Bank of America’s internal Erica is used by 90%+ of employees for HR documentation, password resets, and benefit inquiries. It reduced IT service desk calls by 50%. This is a knowledge retrieval tool—helpful, but not autonomous.

- Morgan Stanley’s Debrief generates meeting notes and converts advisor notes into emails. 98% of advisors use a chatbot trained on all of the company's intellectual data. Again, useful automation—but the human drives every interaction.

- Lloyds Banking Group’s Athena serves 20,000 employees as an internal knowledge base, reducing search times by 66%. An HR assistant answers 90% of employee queries correctly on the first attempt.

True agents (autonomous, multi-step):

- Citibank’s AI automates code reviews, freeing up 100,000 developer hours a week—the equivalent of 2,500 full-time developers. AI independently reviews, flags issues, and processes code without step-by-step human prompting.

- Allianz's “Project Nemo” uses seven AI agents to detect fraud and automate insurance claims, reducing processing time by 80%. For food spoilage claims under AUD$500, processing dropped from several days to hours.

- BNY Mellon has 134 “digital employees,” which are AI agents with defined roles that work 24/7 on specific repetitive tasks. Some of their jobs were done by humans last year.

“The digital employee works 24/7, which is obviously very different to our human counterparts. It's really focused on very specific repetitive tasks that allow our human employees to do much more human, intense, interesting-type roles,” says Rachel Lewis, head of payment operations at BNY.

Takeaway: Financial firms are spending loads of money on building their own AI agents internally to improve employee productivity and reduce costs. But there’s a wide gap between a chatbot that answers questions and an agent that independently executes workflows. The firms getting the most value are the ones deploying AI that actually does things autonomously (code reviews, claims processing, payment operations), not just the ones that answer questions faster.

Client experiences are getting more personalized and efficient due to AI

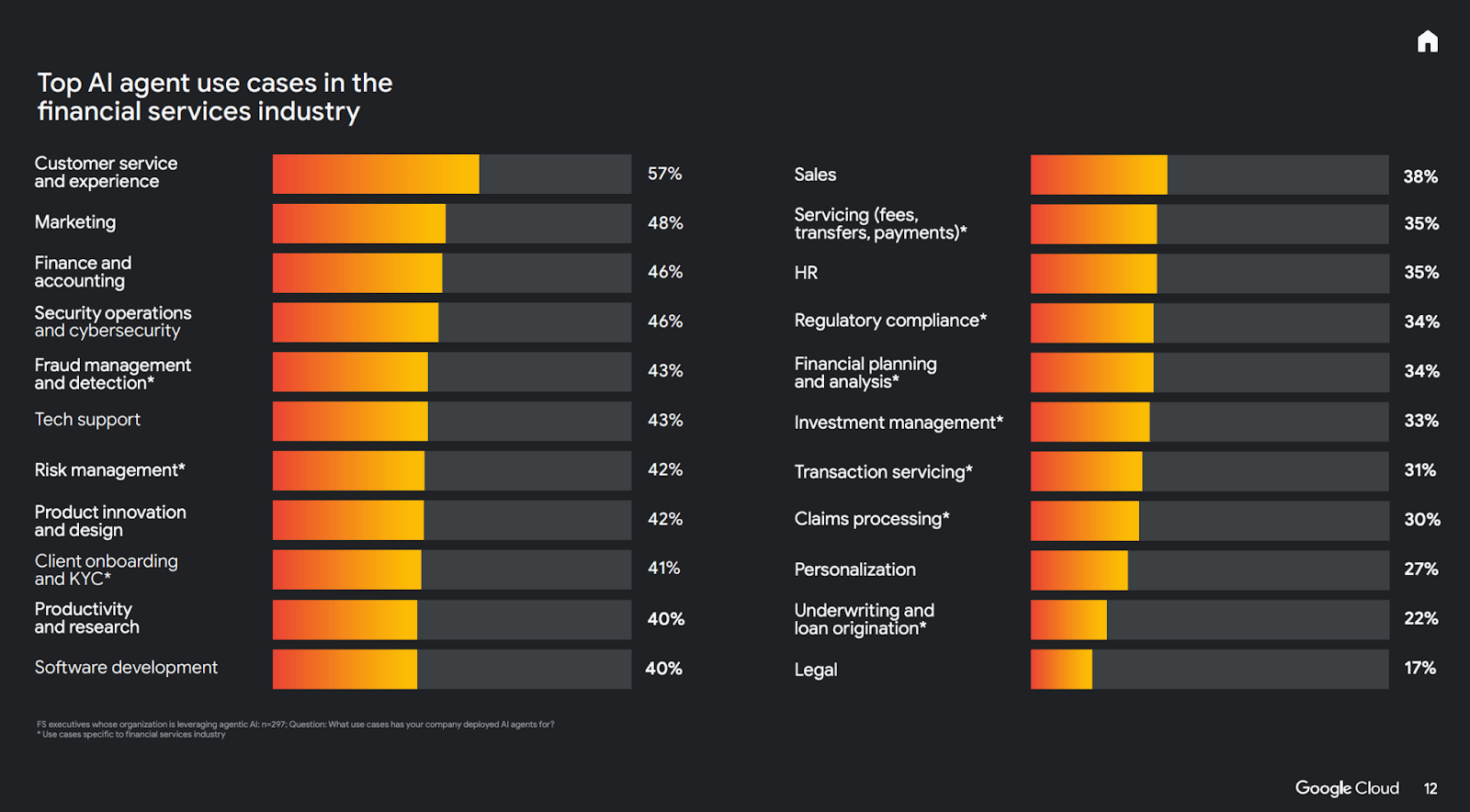

To no surprise to anyone, the finance industry (like tech, healthcare, and every other sector in the world) is also using artificial intelligence to improve customer experience. Google Cloud’s report about ROI of AI in financial services also found improving customer experience via AI agents as the top use case.

The best way to enhance customer satisfaction for financial firms specifically is to:

- Improve the bottlenecks that often surround financial tasks for people

- Provide a more tailored and personalized experience

For Bank of America, this effort started by launching Erica—yes, the same AI agent it uses for employees also has a customer-facing side to the coin. Since its launch, it has surpassed 50 million users and over three billion client interactions. This is the equivalent work of 11,000 staffers daily.

“Our clients appreciate Erica’s ability to help them manage their spending, improve budgeting and increase savings. Erica is the bedrock upon which we’ve built an unmatched high-tech, high touch client experience,” says Nikki Katz, head of digital at Bank of America.

Insurance company Lemonade also relies on several AI agents to serve clients better and faster. AI chatbot Maya helps new prospective clients find the right policy for them and AI Jim processes claims the company receives from its customers at whip speed—approx 40% of claims are resolved within minutes.

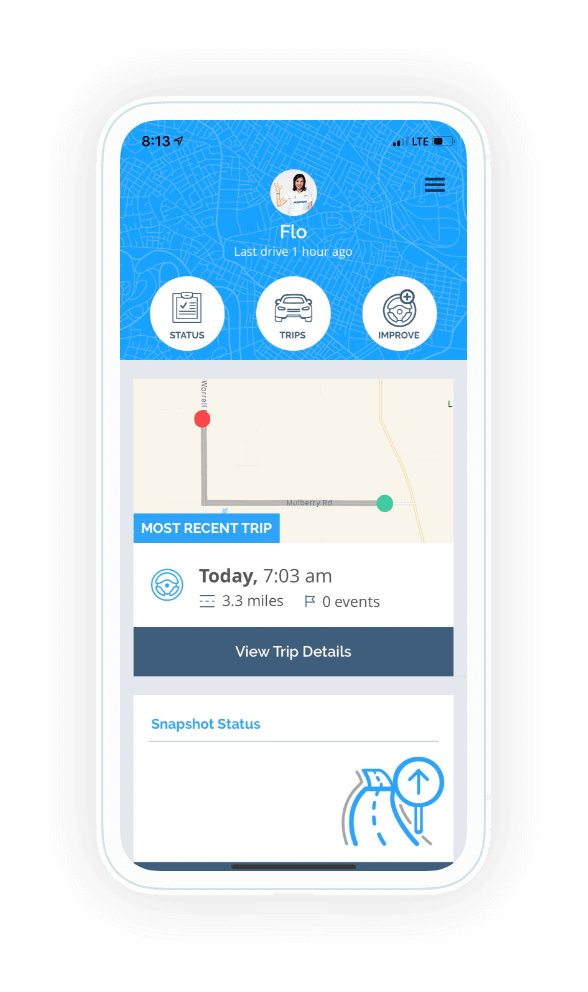

Progressive, another insurance company, also has several AI agents to make its customers’ lives easier. One in particular—that garnered a lot of attention and love—is Snapshot. It personalizes your car insurance rate based on your driving, aka usage-based insurance. According to the company, drivers using Snapshot save $322 a year.

Klarna also has impressive achievements to rave about. The BNPL company’s AI customer service agent has saved the company a whopping $60 million and now does the work of 853 full-time agents.

Wells Fargo’s AI assistant also handled over 245 million customer interactions without human intervention in 2024—more than double the company’s original projections.

JP Morgan is also looking to use IndexGPT to offer thematic investment advice tailored to individual cash flow patterns.

Takeaway: Financial firms across the board are using artificial intelligence to improve the customer experience—whether that’s by resolving queries faster or sharing personalized offers. Most large companies have been doing some version of this for years, but AI has accelerated their efforts.

AI isn’t causing mass layoffs, but it’s reshaping who gets hired

The “AI is killing banking jobs” narrative is mostly overblown. The data doesn't support mass layoffs:

- Bank of America employed just four fewer workers at the end of Q3 2025 compared to 2024

- Goldman Sachs (despite multiple layoff rounds) added 1,800 more employees

- JPMorgan added 2,000 employees

But the real story isn't in the total headcount. It's in who is getting hired—and who isn't.

The biggest shift is at the bottom of the ladder. Big firms are reportedly considering pulling back entry-level hiring by as much as two-thirds as they rely more on AI.

- Bank of America hired just 2,000 recent grads from 200,000 applications—a 1% acceptance rate

- Goldman Sachs accepted fewer than 1% of 300,000 applicants for entry-level jobs last year

The MBA pipeline tells a similar story. In 2021, just 4% of graduates from Harvard Business School didn’t have a job three months after graduation. Today, that number is 15%. MIT witnessed a near identical jump from 4.1% in 2021 to 15%.

21% of Duke University’s graduates and 15% of those at Michigan University also remained on the hunt for a job three months post graduation.

Many financial firms are also planning to reduce headcount as AI helps automate many tedious jobs.

- Citigroup has already laid off 1,000 employees and plans to push that number to 20,000 by the end of 2026. This would be about 8% of the company’s global workforce.

- JP Morgan, too, has predicted a 10% reduction in its workforce in the next five years due to automation. This is primarily in operational roles that deal with tasks like fraud detection or account setup.

- Wells Fargo has also aggressively made cuts in its staff—the company’s workforce has fallen from nearly 217,500 in December 2024 to about 205,200 today.

These actions are in line with Bloomberg Intelligence’s estimations (done in 2025): Global banks could shed up to 200,000 jobs over the next half a decade as AI spreads into core operations. The roles likely to be most exposed are back-office, middle-office, and operational functions—functions where repetitive processes dominate.

It’s worth remembering that the dominant strategy of financial firms isn't firing people—it's not replacing them when they leave. Finance teams—like that of JP Morgan—are experimenting with absorbing employee attrition with AI. Bank of America's CEO put it plainly:

“We can just make decisions not to hire and let the headcount drift down.”

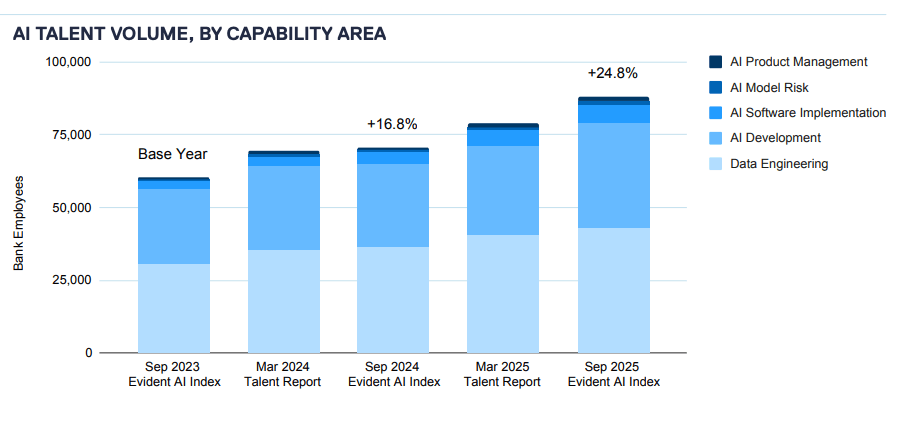

If this sounds like all hope is lost, hold your breath. AI is also adding more jobs. While overall banking headcount declined 3% between 2023 and 2025, AI-specific roles grew from 60,000 to nearly 80,000. The largest banks increased their AI talent pool by 13% in just six months—the biggest jump in two years.

According to Evident Insights’ annual report on 50 of the largest global financial firms, the AI talent pool grew by 25% YoY.

The top five banks expanding their AI talent were Capital One, JPMC, Citigroup, Bank of America, and Wells Fargo.

Takeaway: The financial sector isn't seeing mass layoffs—it's seeing a slow-motion workforce recomposition. Entry-level and operational roles are being absorbed by AI, while demand for AI engineers, data scientists, and ML specialists is surging.

The ROI of AI financial firms

This is arguably the most important question for any financial firm investing in AI: is it actually worth it?

The honest answer, for most firms, is…not yet.

According to BCG's 2025 survey of 280+ finance executives, the median ROI from AI in finance is just 10%—well below the 20% many firms are targeting. Only 45% of executives can even quantify their ROI. And about a third report returns under 5%.

The Caspian One report paints a similar picture: only 38% of AI projects in finance meet or exceed ROI expectations, with implementation delays averaging 14 months.

There are three reasons why most financial firms are stuck below 10% ROI:

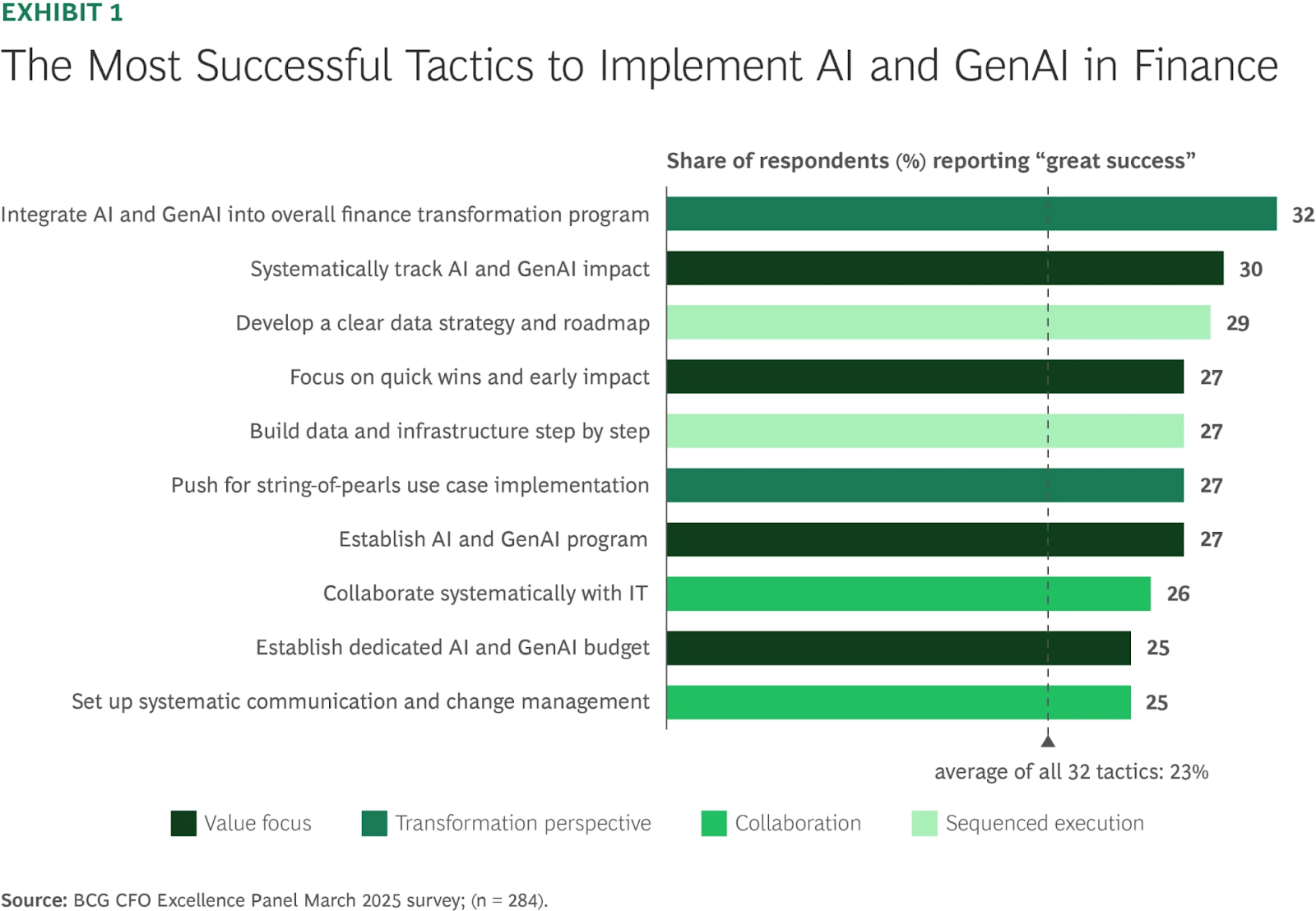

- Too many disconnected pilots, not enough scaled deployments. The typical finance function has six use cases in proof-of-concept and five in production. But few have more than ten active total. BCG found that teams that embed AI into their overall finance transformation increase their probability of success by 7% over those running scattered pilots.

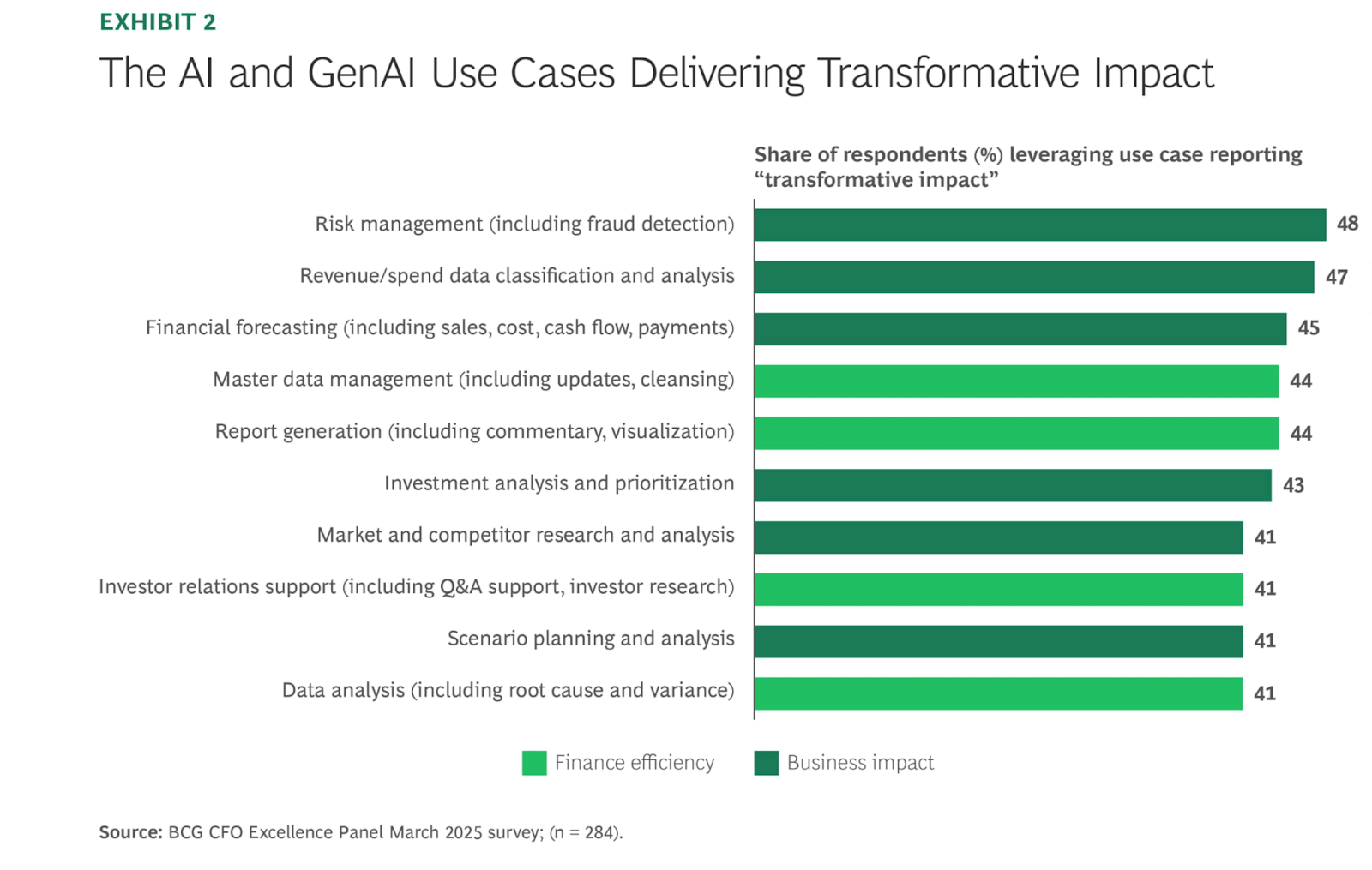

- The wrong use cases get prioritized. Most teams focus on internal efficiency—payables, receivables, policy drafting, and coding. These are faster to implement but deliver modest returns. BCG’s data shows the highest-ROI use cases are in risk management and financial forecasting—areas many firms haven’t even started exploring with AI.

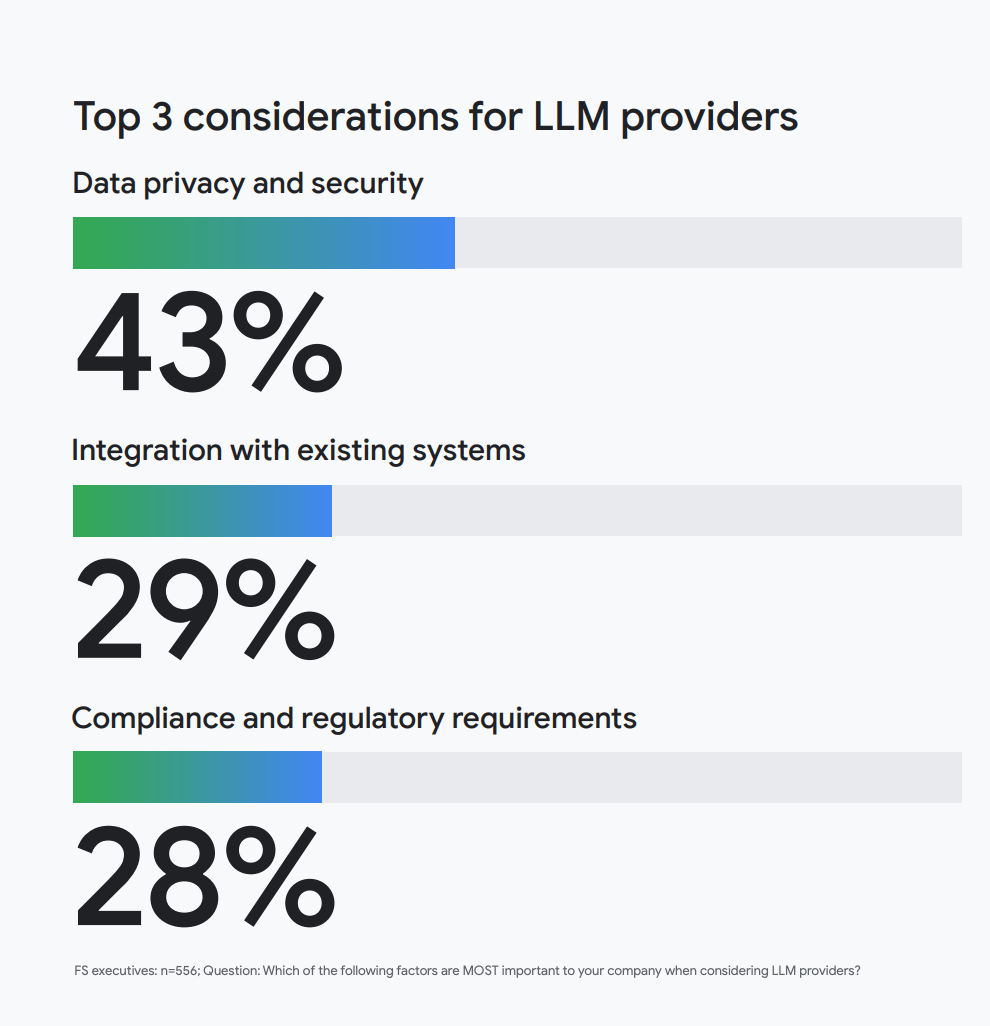

- Compliance, regulation, and auditability slow everything down. Finance teams face more implementation hurdles than other functions. Google’s research tracks with this—data privacy, compliance, and integration with existing systems are the key challenges of implementing AI in financial services.

But here's the counterintuitive finding: the firms with the strongest governance are also the ones seeing the best returns. EY found that companies with real-time AI monitoring are 34% more likely to see revenue growth improvements and 65% more likely to see cost savings than firms without it.

DBS is the clearest example. It operates under a “PURE” framework—every AI system must be Purposeful, Unsurprising, Respectful, and Easy to explain. For high-risk applications, DBS has automated kill switches that activate if any performance metric is breached.

The takeaway isn't that regulation doesn't matter. It's that the firms treating governance as a strategic investment—not a compliance checkbox—are deploying faster and getting better returns than the ones treating it as an obstacle to be minimized.

Despite these hurdles, one in five finance teams still manage to report 20%+ ROI from their AI and genAI investments. Here are three examples:

- JP Morgan, for one. As we discussed, they’re breaking even on their $2 billion AI investment.

- DBS bank, too, realized a whopping $1 billion in value from AI initiatives in 2025. The bank has over 1,500 AI models across more than 370 use cases—primarily for client support, fraud prevention, and coding assistance.

- Lloyd Banking Group also highlighted £50 million ($68.7 million) of value in 2025 from artificial intelligence. Similar to DBS, Lloyd also uses AI for customer support, coding, and internal operations. In 2026, the org expects £100 million ($137.4 million) in additional value from AI.

What are these firms doing differently?

- They go big on back-office first, then expand. The most successful AI deployments in finance aren't in flashy, customer-facing tools—they're in back-office operations where high volume meets repetitive workflows. Fraud detection, compliance screening, document analysis, and code generation consistently deliver the highest ROI.

Bank of America, for example, started with Erica for Employees handling IT support calls, then expanded outward. - They integrate AI into existing systems: Instead of treating AI as a standalone tool for various different tasks, zoom out and take a broader perspective. String together various use cases and analyze how you can embed AI into the overall finance transformation agenda.

- They track AI impact obsessively: You can’t improve what you don’t measure. Set clear aims of what you hope to achieve with each AI initiative you pilot and measure it regularly to assess which efforts are worth it and which are a waste. DBS, for example, publishes AI value in audited annual reports.

These recommendations are in line with what BCG recommends as the most successful tactics to implement AI in finance.

- They hire AI specialists: The Caspian report found 65% of financial institutions experience implementation delays averaging 14 months. These delays are primarily driven by shortages in specialised AI talent who understand the nuances of the financial sector. If that’s not enough, the research also found AI with specialist teams see up to 60% efficiency gains and 40% cost reductions in areas like onboarding, compliance, and settlement. Hire AI specialists who also have a background in finance to strike gold.

Takeaway: The ROI gap in financial AI is real—but it’s not a technology problem. It’s an execution problem. The firms hitting 20%+ returns are starting with high-impact back-office use cases, integrating AI into their transformation strategy instead of running isolated pilots, measuring everything, and hiring people who understand both the tech and the industry.

Where do financial firms go from here?

This report makes it clear AI is a non-negotiable part of the finance sector, and it’s definitely restructuring the industry.

The easy wins are already showing returns: better fraud detection, personalized customer experience, time savings in operational work, and cost savings in repetitive work. What’s next?

The challenge finance firms face now is balancing AI usage with data privacy and compliance policies. A lot of the future will depend on new and rare skills of AI specialists who also understand the intricacies of finance.

The next wave of value in financial AI is in forecasting, risk modeling, and decision-making. That's harder to build, measure, and hire for. But the firms that crack it will operate fundamentally differently.

.png)